UK Spring Statement 2026: Key analysis

Economics Views & insightsWe analyse the measures announced in the UK Spring Statement and how they could impact personal finances, investments and the wider economy.

3 March 2026 | 8 minute read

Key highlights

- Stability over surprises: The chancellor has prioritised predictability. No new tax changes mean a more stable environment for wealth planning.

- Conflict in the Middle East: Disruption is driving energy price speculation. Sustained rises could impact utility bills and inflation, testing the government’s fiscal headroom.

- Navigating the ‘frozen’ years: With personal tax thresholds on hold until at least 2031, proactive planning reviews are vital to manage the hidden impact of fiscal drag on your income.

After last November’s tax-raising Autumn Budget, today’s Spring Statement took a markedly different approach. This was an economic update, not a fiscal event – in wealth planning terms, that’s welcome news.

The chancellor opted for stability over surprises. No major tax changes. No sweeping policy shifts. Instead, the focus remained on existing plans and updated economic forecasts from the Office for Budget Responsibility (OBR). However, this stability sits against a volatile backdrop. The OBR warned that the evolving Middle East conflict could lead to a ‘very significant’ hit to the UK economy.

So what are the implications for your wealth strategy in 2026? Our analysis examines the Spring Statement’s relatively limited measures affecting personal wealth and investments, while Guy Foster, Chief Strategist, evaluates the UK’s economic prospects in light of the OBR’s latest projections and the ongoing conflict in the Middle East.

The health of the UK economy

The good news from the Spring Statement is that the current trajectory of the public finances remains broadly consistent with the plans laid out at the Autumn Budget last November. However, there’s a sense in which this statement and these forecasts have been overtaken by the conflict in the Middle East.

The reality of fiscal rules

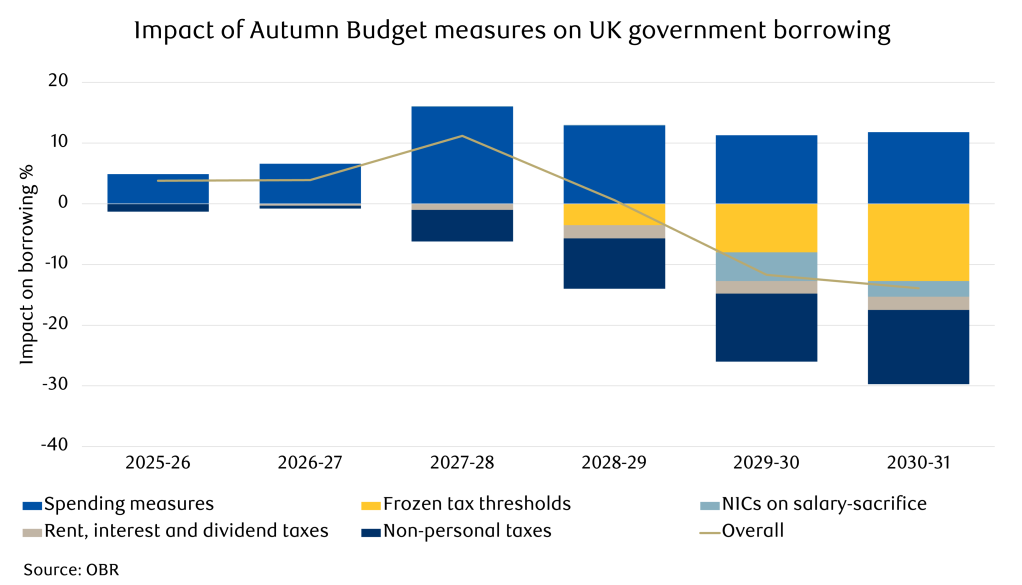

During the Autumn Budget, measures were announced which reduced public sector net borrowing. However, these cuts aren’t scheduled until 2029 to 2031. While this plan complies with the government’s fiscal rules, it serves more as a signal of intent than a guarantee.

As a reminder, the chancellor has committed to fiscal rules designed to keep government borrowing at a sustainable level. These rules state that by 2029/30:

- Current spending must be less than government revenue.

- Debt should be falling as a share of annual economic activity.

Last autumn’s announcements make meeting these fiscal tests likely, though the margin for success is narrow. Furthermore, the planned cuts to borrowing wouldn’t take place until 2029.

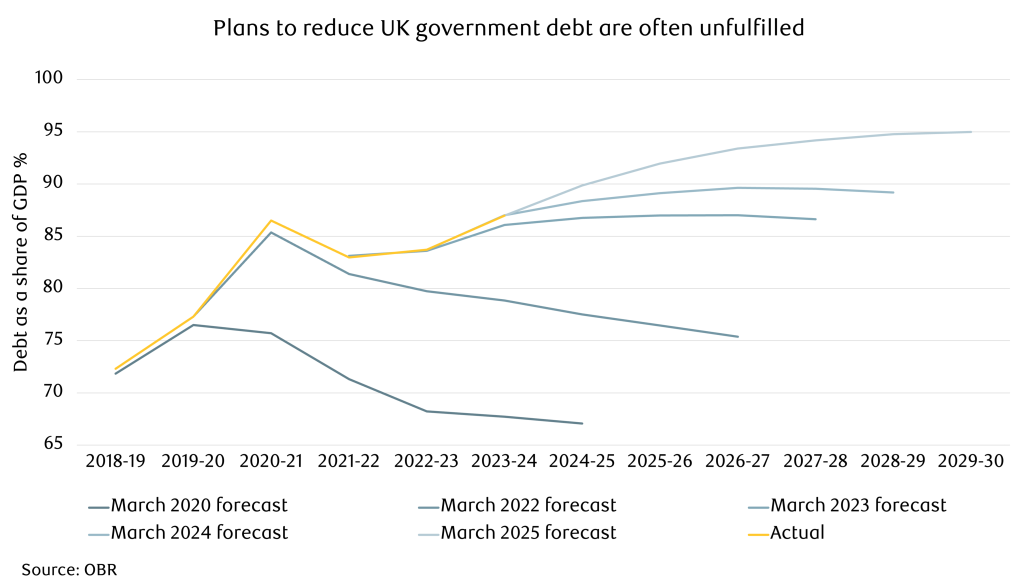

The OBR warned again that governments have tended to reverse plans to strengthen the public finances. The annual tradition of delaying the planned increase in fuel duty is an example of how political necessity outweighs fiscal prudence. However, the most significant reversals are often forced by economic shocks, such as the pandemic or the energy crisis.

Ironically, the difficulty of abiding by previous fiscal plans is what could limit the government’s ability to cope with any new economic shocks.

We see this today as the Middle East conflict damages energy infrastructure, driving prices higher. With Qatari gas typically destined for Europe, these disruptions have sparked speculation of sustained price rises. You can read our investment analysis on the unfolding conflict here.

Looking ahead

Sustained gas price rises would eventually impact domestic utility bills. There’s certainly potential for higher inflation and the ensuing lower growth to overwhelm the government’s modest fiscal headroom. As a result, it could come under pressure to provide subsidies, similar to the measures seen between 2022 and 2024.

In the bond market, government bond yields rose following the Spring Statement, likely in anticipation of fewer interest rate cuts and potential increases in borrowing caused by the disruption to the energy market in the Middle East. However, assuming the U.S. can neutralise Iran’s ability to harass energy production and transit, prices could return to normal.

There are many parties with a vested interest in getting that energy flowing once more, although a protracted conflict could start to impact domestic energy prices and UK public finances.

Your wealth strategy

The certainty provided by Chancellor Reeves is valuable: personal tax thresholds won’t change again until at least the next Autumn Budget. While the Spring Statement itself had limited impact on personal finances, substantial changes are already scheduled over the coming years. This creates a clear window to implement strategies before tax year-end and work with your adviser on any remaining opportunities from last autumn’s announcements.

We’ve outlined some of the key deadlines and considerations for your wealth planning below. For a full breakdown of these changes, see our Autumn Budget 2025 analysis.

Before April 2026

- Review your estate plans: New caps are coming for Agricultural and Business Property Relief. For qualifying assets, a combined limit of £2.5 million per person (or £5 million for married couples and civil partners) will apply for 100% inheritance tax (IHT) relief. Anything above this may be taxed at an effective IHT rate of 20%. Additionally, stocks listed on the Alternative Investment Market (AIM) will be subject to IHT at a rate of 20%, regardless of the value held.

- Consider lifetime gifting: Now is an excellent time to explore gifting strategies. Helping your loved ones now can support them during your lifetime while also potentially reducing your future IHT bill.

- Act on investment tax relief: If you use Venture Capital Trusts (VCTs), the income tax relief is set to drop from 30% to 20% on 6 April 2026. You may want to talk to your adviser about making the most of the current rates.

- Prepare for dividend changes: Tax on dividend income is rising by 2% for both basic and higher-rate taxpayers. There is no increase to the dividend tax rate for additional rate taxpayers, who will continue to pay at 39.35% during the 2026/27 tax year. Reviewing how you receive your income now could help you manage any future increases.

Before April 2027

- Pensions and IHT: From April 2027, unused pension funds will generally be included in your estate for IHT purposes. This is a significant shift, as many people currently use pensions as a tax-efficient way to pass on wealth. You may wish to consider how this fits into your wider plans and whether the existing death benefit nomination (determining who the beneficiaries of pension funds are as this isn’t covered in a will) needs to be amended or not.

- Withdrawal strategies: You might find it helpful to look at whether taking pension lump sums now could help manage your future tax exposure.

- New tax rates for savings and property income: From April 2027, tax rates for both savings and property income are set to rise by 2% across all bands. This includes a new, separate tax structure specifically for UK landlords. The updated rates will be:

- Basic rate: 22%

- Higher rate: 42%

- Additional rate: 47%

- Max out your ISAs: Your overall annual ISA allowance remains at £20,000, though the specific Cash ISA limit for those under 65 will be reduced to £12,000 from 6 April 2027. Balancing income and assets between partners could help you to leverage both allowances.

Before April 2028

- The ‘mansion tax’ surcharge: A new High Value Council Tax Surcharge (HVCTS) is expected for properties worth £2 million or more.

- Restructure your portfolio: You could consider whether changing how you own high-value homes might help manage these extra costs while still preserving your property wealth.

Before April 2029

- New salary sacrifice cap: From April 2029, only the first £2,000 of your salary sacrificed for pension contributions will be exempt from National Insurance Contributions (NICs). If you currently use this strategy to build your retirement pot, it’s worth reviewing your approach before the deadline.

Long-term: Navigating the ‘frozen’ years

- Frozen thresholds: Personal allowances, higher rate thresholds, IHT bands are all frozen until April 2031. While it might feel like things are standing still, fiscal drag means you could pay more tax as your assets and income grow, even if the rates stay the same.

- Regular reviews: Because asset values often grow while tax thresholds stay flat, regular reviews with your adviser are more valuable than ever.

Plan ahead with confidence

We can support you through periods of change and stability to maximise opportunities for your wealth and ideas for the future. The Spring Statement may have been limited in its scope, but the clear timeline on tax changes provides a strong foundation for your wealth planning. Meanwhile, we continue to monitor developments in the Middle East and their potential impacts on portfolios.

If you would like to discuss your plans for the future, please get in touch.

Please note: Information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness. The information provided should not be mistaken for formal planning advice; it is imperative that you seek relevant advice for your own personal circumstances. RBC do not provide tax or legal advice and we would recommend that you seek appropriate advice in these areas. Rates of tax will be based on individual circumstance and tax rules are subject to change. The value of investments, and any income from them, can fall and you may get back less than you invested. Neither simulated nor actual past performance are reliable indicators of future performance. Information is provided only as an example and is not a recommendation to pursue a particular strategy.