UK markets are under the spotlight

Views & insightsUK markets are under pressure. Guy Foster unpacks the politics, the Strait standoff, and what it means for investors.

Key highlights

- UK political uncertainty: As Sir Keir Starmer holds on to his position as prime minister, the rise of potential challenger Andy Burnham unnerves bond markets.

- Strait standoff: Iran’s oil export halt tightened markets and drove up inflation.

- U.S. inflation: April’s consumer price index (CPI) accelerated, but underlying details suggest less cause for alarm.

UK politics: Leadership uncertainty weighs on gilts

The UK was firmly in the spotlight last week as the prospect of a new prime minister looms. Its most pressing challenges have largely been imported – but domestic political pressure, building quietly for months, is now demanding a response.

Local election results confirmed heavy losses for Labour, with Reform and the Greens the main beneficiaries. By Tuesday, Polymarket odds of Keir Starmer being replaced by the end of June had risen above 60%.

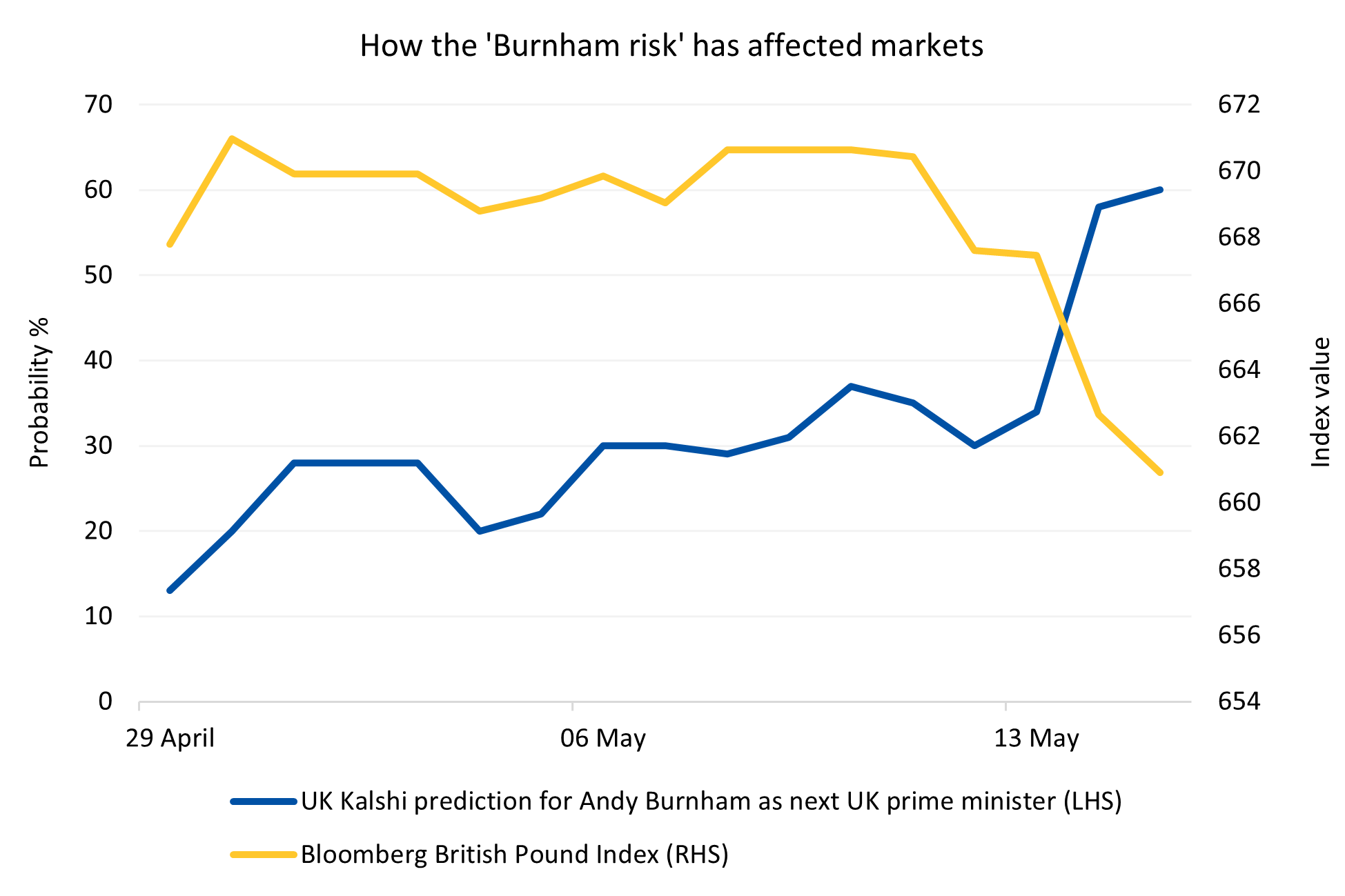

As for his potential challengers, Wes Streeting has resigned from the cabinet, Angela Rayner confirmed she’s been cleared by tax authorities following an investigation, and Andy Burnham has secured a path to a parliamentary seat – via a by-election he’s expected to win. The latter development coincided with a sharp sterling depreciation.

Markets are uneasy about Burnham for identifiable reasons. He’s spoken publicly about moving beyond being “in hock to the bond markets” and has described deregulation, privatisation, austerity and Brexit as “the four horsemen of Britain’s apocalypse.” He’s also signalled ambitions to recapture public control over housing, energy, water, rail and buses.

However one views these positions, reversing them would require substantial spending and carry execution risk – precisely the combination that makes bond investors nervous. Prediction markets give Burnham a 60% chance of success.

Source: Bloomberg

The UK’s first quarter GDP data provided some positive offset, coming in at 0.6% quarter-on-quarter and generally quite strong, with March showing 0.3% growth against expectations of a modest contraction. This suggests UK consumers were able to weather the increase in energy costs during March – probably because UK households raised their savings rates last year to withstand tough economic conditions.

This resilience may reinforce the case for the Bank of England (BoE) to increase rates this year. However, this must be weighed against indications that the housing market is weakening, and survey data suggesting more recent retail sales are likely to be weaker.

The BoE is expected to raise rates at least twice this year, and UK 10-year government gilt yields topped 5.1%, which is higher than 2022 levels. Most of this relates to the prolonged increase in energy costs and impact on inflation, but the political drama is clearly causing some underperformance from UK bonds.

Strait standoff tightens as Trump-Xi talks disappoint

While political drama may be brewing at home, the Iran-U.S. war remained the most important issue across markets last week, with hopes of a diplomatic breakthrough fading as the days progressed. Early last week, the lack of progress in nuclear talks between the U.S. and Iran pushed energy prices higher and weighed on European equities.

By mid-week, satellite imagery confirmed that oil shipments from Khargh Island – Iran’s primary export terminal – had dropped to zero for the longest stretch since the war began, indicating that available floating storage is running out. If Iran exhausts its remaining capacity, it will be forced to cut production outright, which has been a stated aim of the Trump administration’s blockade of the Strait of Hormuz.

Oil prices climbed roughly 8% over three sessions as the physical market tightened. This fed directly into inflation data. The U.S. producer price index (PPI) rose 1.4% month-on-month in April – the largest monthly gain since March 2022 and far above the 0.5% consensus. The annualised figure hit 6%. While the PPI is inherently more volatile than consumer prices, a miss of this magnitude signals that cost pressures are moving through supply chains.

The Japanese PPI told a similar story, marking its fastest year-on-year rise since 2023, driven by oil and naphtha (a liquid hydrocarbon mixture derived from crude oil or other natural sources, which is often used as a fuel, solvent, and petrochemical feedstock) costs – unsurprising for a country that imports 90% of its crude from the Persian Gulf.

The Donald Trump-Xi Jinping summit in Beijing, which had been a source of cautious optimism, delivered little of substance. President Trump asserted the U.S. doesn’t need the Strait of Hormuz open. He did discuss progress on achieving trade deals with China, including vague intentions for China to purchase U.S. oil and agricultural products and a commitment for China to buy U.S. aircrafts.

Where specifics were mentioned, they underwhelmed. The one notable development was the clearing of Chinese tech groups to purchase Nvidia’s H200 chips, which gave a brief lift to NASDAQ futures. Nvidia’s Jensen Huang joining the trip at the last minute now appears to have been the main event.

Against this backdrop, U.S. equities continued their remarkable bifurcation. Tech and AI names drove another strong session on Thursday, with Cisco jumping 20% after hours on an upgraded sales outlook. The broader market, however, struggled with the inflation data – treasuries sold off, with the 10-year yield reaching almost 4.5%, and the 20- and 30-year yields both closing above 5%.

The U.S. Senate’s narrow confirmation of Kevin Warsh as the next Federal Reserve (the Fed) Chair (54-45, almost entirely along party lines) adds another variable. His first meeting in June will be closely watched, though he’s unlikely to have sufficient data clarity to support any rate move in that timeframe. What’s notable is that since the nomination process began, market expectations have shifted from rate cuts to rate increases. If the new chair doesn’t manage to cut interest rates, history suggests he might receive criticism from the president.

Inflation: Punchy but not panic-inducing

The U.S. CPI for April showed headline prices accelerating to 3.8% year-on-year – the highest since the post-COVID-19 spike. Core CPI rose 0.4% month-on-month, the first upside surprise in several months. However, the detail was less alarming than the headline.

The jump in shelter costs was largely a statistical quirk from the government shutdown last autumn, which caused a full year of accumulated rent increases to appear in a single month’s data. Alternative measures of rental inflation, including the Zillow index, continue to decelerate. Core goods inflation showed surprisingly little tariff pass-through, and Bloomberg Economics assessed that the impact from the ‘Liberation Day’ tariffs is now mostly complete.

The areas to watch are food prices – where fertiliser supply disruption through the Strait poses an upside risk – and semiconductor-driven tech inflation, where Samsung has warned of further market tightening next year.

Household inflation expectations have edged up modestly, but not to levels that would alarm the Fed. We expect the new Warsh-led Fed to remain in wait-and-see mode, with neither a bias to hike nor cut.

Coming up

- Earnings season’s climax: There are few surprises left this earnings season, but Nvidia’s result this week will still be a key focus.

- UK employment: Jobs and wage data will help the BoE’s Monetary Policy Committee decide what action is required.

- UK inflation: How fast did prices rise during April?

The value of investments, and any income from them, can fall and you may get back less than you invested. Neither simulated nor actual past performance are reliable indicators of future performance. Investment values may increase or decrease as a result of currency fluctuations. Information is provided only as an example and is not a recommendation to pursue a particular strategy. Information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness. Forecasts are not a reliable indicator of future performance. We or a connected person may have positions in or options on the securities mentioned herein or may buy, sell or offer to make a purchase or sale of such securities from time to time. For further information, please refer to our conflicts policy which is available on request or can be accessed via our website at www.brewin.co.uk.