Inflation risk, cash and investment reserves

Investing Views & insightsSteep price rises can affect charities in several ways.

27 October 2022 | 3 minute read

By Vicky Eastwood, Charity Investment Manager, RBC Brewin Dolphin

High inflation means it’s more important than ever for charities to review their reserves policy and consider ways to mitigate the impact of price and wage increases on their long-term objectives.

The latest figures from the Office for National Statistics show UK inflation, as measured by the consumer prices index (CPI), rose to 10.1% in the 12 months to September1.

Steep price rises can affect charities in several ways. Charities reliant on providing food and using travel will see a direct impact in their accounts. Demand for some charities’ services is likely to increase as households struggle with the rising cost of living. Research suggests that for the poorest households, who spend a larger proportion of their money on food and energy, the rate of inflation is even higher. In June, for example, the CPI including owner occupiers’ housing costs stood at 8.7% for low-income households, versus 7.8% for high-income households and 8.2% for all households2.

We are also already seeing expectations from employees that their wages will increase to compensate for inflation. Known as wage inflation, a shortage of workers in some areas is making this even more acute. For charities, wage inflation is particularly challenging as employees across the board are being attracted by higher salaries elsewhere.

What does inflation mean for cash reserves?

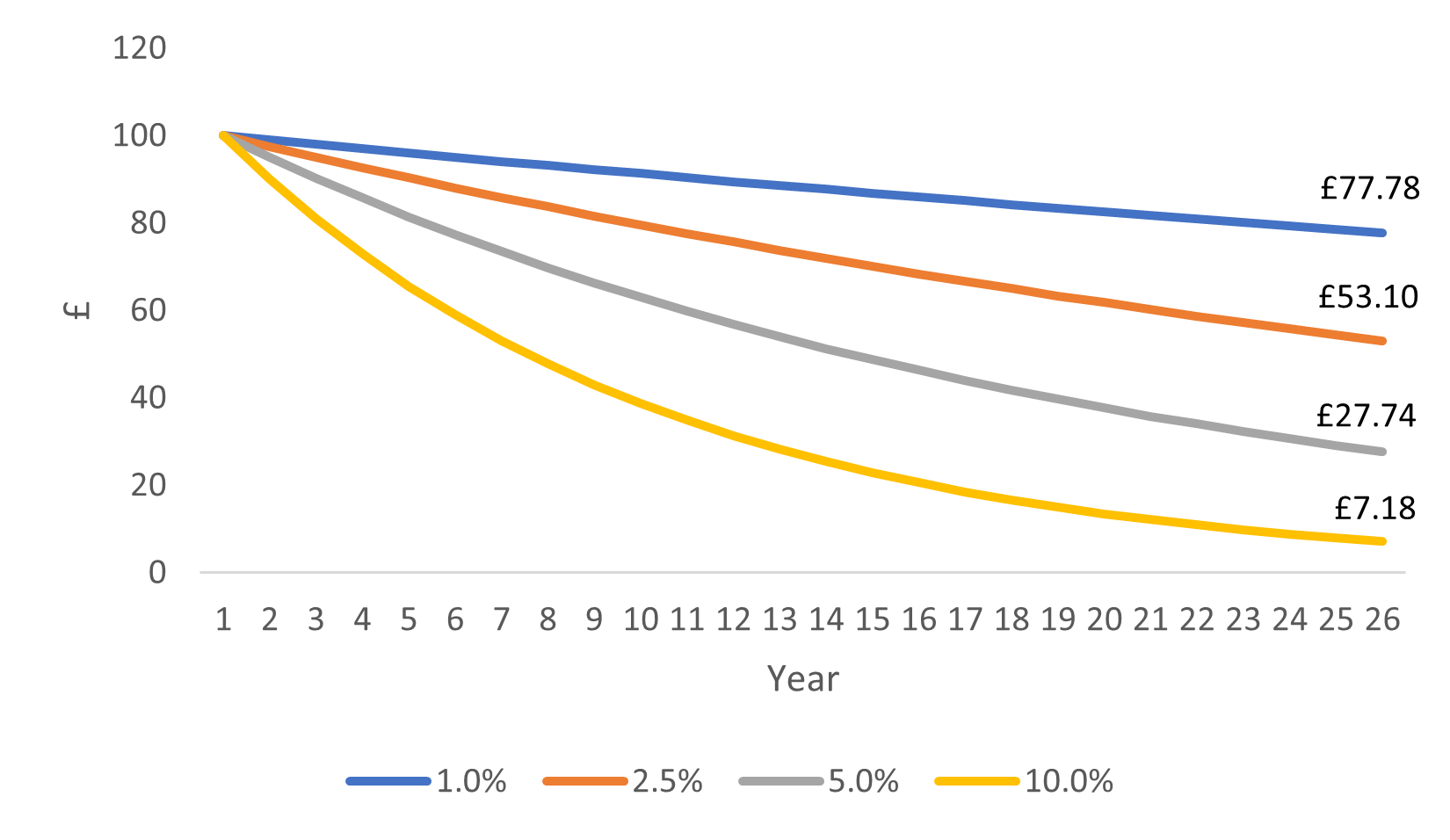

Last but not least, high inflation means cash could be losing its value in real terms. Although interest rates are rising, at a faster rate than they have for many years, they remain below the current rate of inflation. RBC Brewin Dolphin’s own research shows the impact of leaving £100 in a zero-interest cash savings account over 25 years. An annual inflation rate of 2.5% would see its real value decline to £53.10 over the period, while a 5% rate would see its real value drop to just £27.74.

Impact of inflation on ‘real’ value of cash

Source: RBC Brewin Dolphin. For illustrative purposes only.

For trustees, who have a duty to protect the real value of their charity’s reserves, it may be worth considering whether part of the cash reserves could be invested with the aim of generating a better return than cash over the long term.

Investing part of your charity’s cash reserves isn’t a decision to be taken lightly and the impact of high inflation may mean that higher levels of cash are required following review. While history shows that investing typically offers better returns than cash over long periods, assets can be subject to fluctuations in value along the way, which might not be suitable for all charities. However, for those who can take a longer-term view with a portion of their reserves, it is worth looking for ways to mitigate the risk of inflation.

Some of the points to discuss and review regularly with your investment manager include:

-

The charity’s overall investment policy and objectives.

-

How to achieve the right balance between risk and return and aligning this with your reserves policy and ‘pots’.

-

Whether to adopt an ethical, socially responsible or mission/purpose related approach.

-

Investing any permanently endowed funds in a way that benefits both short-term and long-term aims.

-

Potential tax implications.

Is now a good time to invest?

Investing your cash reserves may seem counterintuitive when economists are warning of a recession. With economic growth slowing, interest rates rising and consumers experiencing a cost-of-living squeeze, it could be wise to adopt a more cautious stance. However, it’s important to bear in mind that markets are forward looking and that some of the bad news – particularly rapid interest rate increases – has already been priced in to equity valuations. While the pullback in stock markets is unnerving, it has created an opportunity for charities who can afford to take on investment risk to phase funds in.

Having been absent for many years, inflation is back with a vengeance, and it looks like it will be with us for some time to come. The sooner trustees consider its implications and what they might be able to do to offset its effects, the better positioned they will be to deal with it. Investment may not be for all charities, but in an environment where it is more important than ever to make the most of reserves, it is certainly worth considering. Even if the decision is made not to invest, trustees will have been through the due diligence process and will know that it is not right for them at the current time.

The value of investments, and any income from them, can fall and you may get back less than you invested. This does not constitute tax or legal advice. Tax treatment depends on the individual circumstances of each client and may be subject to change in the future. Neither simulated nor actual past performance are reliable indicators of future performance. Information is provided only as an example and is not a recommendation to pursue a particular strategy. Information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness. We will only be bound by specific investment restrictions which have been requested by you and agreed by us. Opinions expressed in this publication are not necessarily the views held throughout RBC Brewin Dolphin. Forecasts are not a reliable indicator of future performance.