10 March 2025

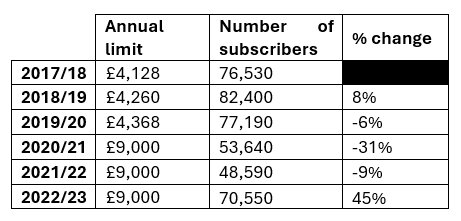

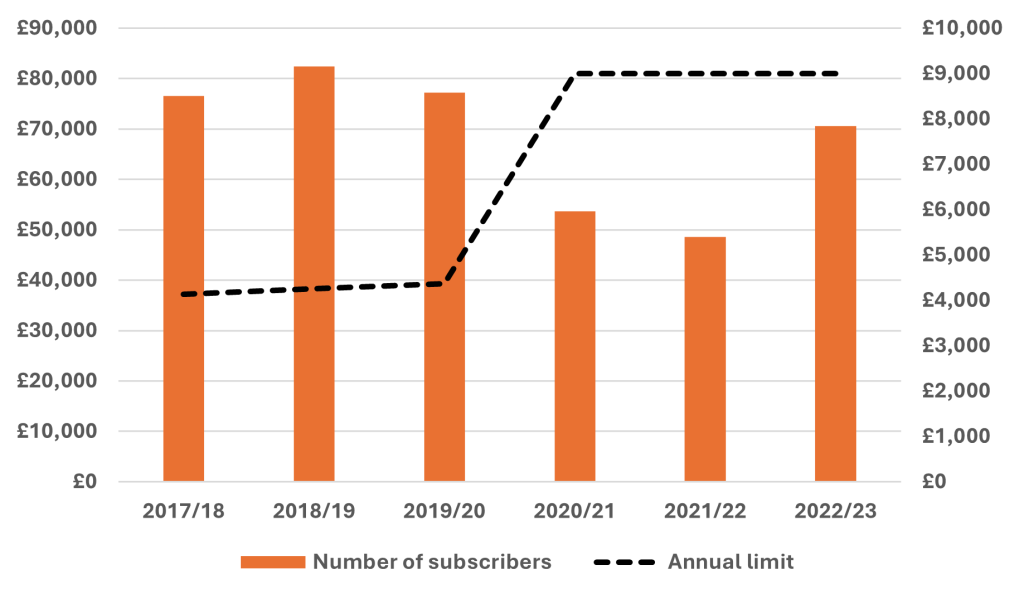

The number of Junior ISA (JISA) accounts that were filled to their maximum annual allowance rebounded strongly during the 2022/23 tax year – the most recently available data – according to figures obtained by RBC Brewin Dolphin.

A Freedom of Information request to HMRC from the wealth manager found that 70,550 people across the UK managed to pay in the full £9,000 during the 2022/23 tax year, compared to 48,590 during 2021/22 – a year-on-year increase of 45%.

Table 1: Number of JISA accounts reaching annual limit:

The large increase has seen the number of savers able to maximise the allowance catch up considerably on the levels recorded when the annual limit was lower, prior to the 2020/21 tax year. During 2018/2019, 82,400 people maximised their £4,260 allowance – the highest rate of recent tax years.

Peak to trough, there had been a -41% decline in the number of people maximising their JISA allowance when the limit was raised to £9,000, but the gap now stands at just -14%.

Figure 1: Number of JISA accounts using the maximum allowance vs annual limit

Source: HMRC, RBC Brewin Dolphin

Anyone can contribute to a JISA account on behalf of a child, providing them with tax-free savings. The child can also take control of the account when they reach 16 years-old but cannot withdraw the money until they turn 18.

Last year, a separate FOI request made by RBC Brewin Dolphin to HMRC revealed that the top 50 child investors were sitting on pots averaging £761,000 in their stocks and share JISAs, putting them firmly on track to join millionaires’ row by their 20s[1].

HMRC’s figures underscore the value of long-term planning and the power of compounding. And while not every family will have the means to amass £500,000 by the time their children head off to university, a more modest pot of £50-£100,000 will certainly be within the reach of many. Starting at birth, a £50,000 pot could be built by the child’s 18th birthday on contributions of roughly £150-a-month, assuming annualised returns of 5% after charges. Increase the contribution to £300-a-month, and the stocks and shares Junior ISA will be looking at a windfall of around £100,000.

The figures for 2021/22 showed the number of children with £50,000+ saved more than doubled compared to the previous year from 8,130 to 16,420, while investors with £100,000+ pots more than trebled from 540 to 1,910. Of those, there were 370 pots in excess of £200,000, compared with just 40 in 2020/21.

Daniel Hough, financial planner at RBC Brewin Dolphin, said: “It is highly encouraging to see more people maximising the use of their annual JISA allowance to support the next generation of their families – they are an incredibly useful tool to help build up a pot that can help with some of life’s big events, whether going to university or taking the first step onto the property ladder. While the doubling of the annual allowance had a big impact on the number of people able to maximise it each year, it looks as though more people are finding the means to do so and pass down as much of their excess income or wealth as possible.

“That said, while some people may be able to maximise it for one or a couple of years, they may not be able to do so consistently. These figures suggest that may well be the case given the large changes even between years where the allowance has been similar. Broadly speaking, grandparents tend to be the ones filling up JISAs where they are fortunate enough to have the free cash to do so. We would generally advise them to maximise their own allowances before looking at others’.

“What we tend to see is grandparents making gifts, which they can do annually up to £3,000 per grandchild – or up to £6,000 for a married couple through their combined gifting allowance – and then do ‘one off’ or a few JISA contributions until their own assets have built back up and they are in a position to pass down more. The difficulty for families with lots of children, and therefore many JISAs, is that it might not be possible to fund them all at the same time.

“Furthermore, there are inheritance issues to take into consideration. It would have been relatively straightforward to make a contribution of, for example, £4,128 and, for cases where the cash was being given by two grandparents, there would have been no Potentially Exempt Transfer (PET) concerns to worry. But, £9,000 is up to £3,000 more than the annual joint gifting allowance, which could lead to complications if the gifter passes away within seven years of the transaction.

“Finally, there is the issue of when a child takes control of their Junior ISA account. Some parents or grandparents may have understandable concerns about an 18-year-old having potentially tens of thousands of pounds at their disposal – or hundreds of thousands, in the most fortunate instances.

“For those who want more control, Junior self-invested personal pensions (SIPPs) could be an alternative. These allow you to still make the financial gift, with the peace of mind that your child or grandchild won’t take control of them until they reach retirement, and it will support them later in life. However, the limit for contributing to a Junior SIPP is lower at £2,880 net, grossing up to £3,600 after government contributions.”

Disclaimers

The value of investments, and any income from them, can fall and you may get back less than you invested.

This does not constitute tax or legal advice. Tax treatment depends on the individual circumstances of each client and may be subject to change in the future.

Neither simulated nor actual past performance are reliable indicators of future performance.

Performance is quoted before charges which will reduce illustrated performance.

Information is provided only as an example and is not a recommendation to pursue a particular strategy.

Information contained in this document is believed to be reliable and accurate, but without further investigation cannot be warranted as to accuracy or completeness.

– ENDS –

PRESS INFORMATION

For further information, please contact:

Siân Robertson: Sian.Robertson@brewin.co.uk / Tel: +44 (0) 20 3201 3026

Payal Nair: payal.nair@brewin.co.uk / Tel: +44 (0) 20 3201 3342

Georgia Embrey: Georgia.embrey@rbc.com / Tel: +44 (0)7704 667 842

NOTES TO EDITORS

About RBC Brewin Dolphin

RBC Brewin Dolphin is one of the UK and Ireland’s leading wealth managers and traces its origins back to 1762. With £57.6bn* billion in assets under management, it offers award-winning, bespoke wealth management services, including discretionary investment management and financial planning.

Its qualified investment managers and financial planners are based in over 30 offices across the UK, Jersey and Republic of Ireland, with a commitment to high standards of client service, long-term thinking and absolute focus on clients’ needs at the core.

As part of Royal Bank of Canada (RBC), RBC Brewin Dolphin is now able to draw on the strength of a global financial institution to enhance the services it provides to clients and to drive further innovation across the business.

*as at 31st October 2024.

Disclaimers

The value of investments can fall and you may get back less than you invested.

RBC Brewin Dolphin is a trading name of RBC Europe Limited. RBC Europe Limited is registered in England and Wales No. 995939. Registered Address: 100 Bishopsgate, London EC2N 4AA. Authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

® / ™ Trademark(s) of Royal Bank of Canada. Used under licence.

ABOUT RBC

Royal Bank of Canada is a global financial institution with a purpose-driven, principles-led approach to delivering leading performance. Our success comes from the 98,000+ employees who leverage their imaginations and insights to bring our vision, values and strategy to life so we can help our clients thrive and communities prosper. As Canada’s biggest bank and one of the largest in the world, based on market capitalization, we have a diversified business model with a focus on innovation and providing exceptional experiences to our more than 18 million clients in Canada, the U.S. and 27 other countries. Learn more at rbc.com.

We are proud to support a broad range of community initiatives through donations, community investments and employee volunteer activities. See how at rbc.com/peopleandplanet.

[1] Source: RBC Brewin Dolphin