Stocks and shares or buy-to-let: what is right for you?

Financial planning Views & insightsBritons are famous for their love of property, and it has been one of the most popular investments of the past 20 years. The appeal of a tangible asset that has the potential to rise in value, in addition to providing a regular rental income, has led around 2.5m people to invest in a buy-to-let property since the market was opened up to private investors in the 1990s.

19 December 2019 | 4 minute read

However, analysis of the financial returns provided by property compared to investing in the stock market make surprising reading. While many property owners have done well, it is the stock market that has been the best performer when viewed over the long term.

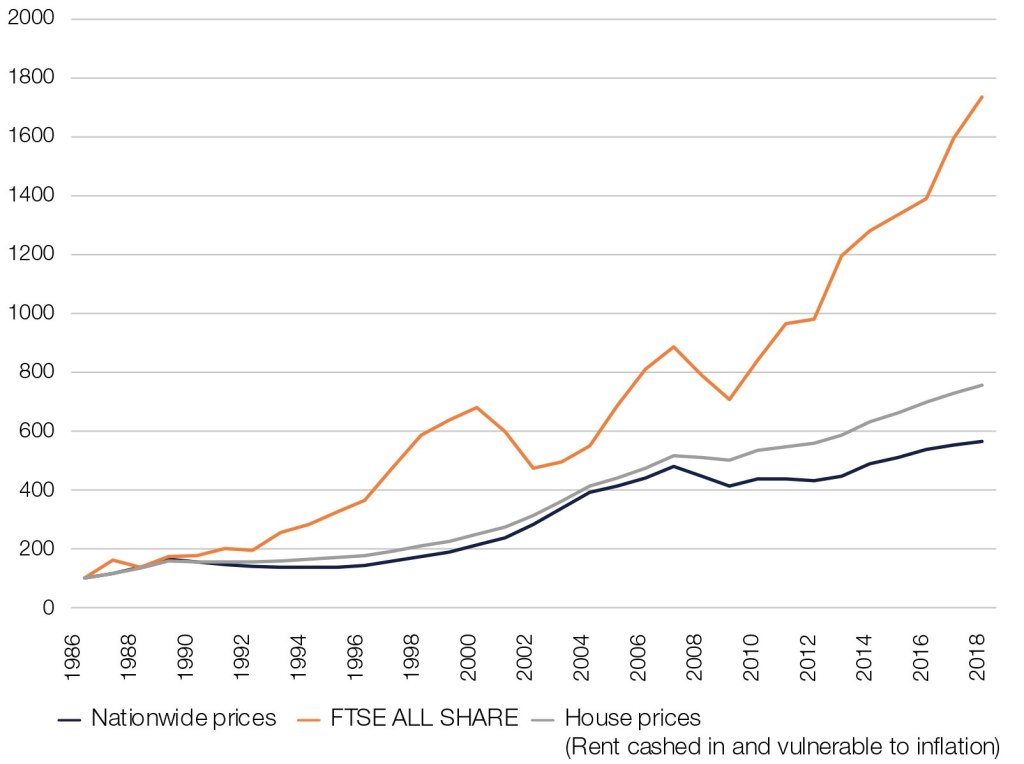

Analysis by Brewin Dolphin shows that somebody who invested £100 in the stock market in 1986 would have accumulated a total of £1,755 to date, through a combination of capital gains and dividends – profits paid out each year by stock market listed companies.

That same sum invested in a buy-to-let property would have produced a return of £739, a relatively modest return of 639%, through a combination of capital growth and rental income.[1]

Nevertheless, many people still love the fact that property is a tangible asset; something they can see and touch, as opposed to stocks and shares, which many people regard as more complex, and risky.

Liz Alley, Divisional Director, Financial Planning at Brewin Dolphin said, “Many people can be nervous about investing in the stock market and investing in the short-term can be risky and volatile. But, with the right financial advice, investing over the long term the stock market can provide solid returns and help you achieve your financial goals.”

Alley adds that recent changes to the taxation of buy-to-let properties have made it far harder to find a property that will turn a decent profit.

“Landlords are finding it hard to get to grips with the fact that they will be prevented from deducting mortgage interest, which is an expense, from their profits, and will instead be given a 20% tax credit on their eventual tax bill” says Alley.

“For higher-rate taxpayers this means effectively paying tax on mortgage interest – in addition to the interest itself. For many people, this just doesn’t make sense”.

The fact is that this tax change has turned many profitable investment properties into loss-making concerns.

Hidden expenses and the hassle factor

Millions of people have invested in buy-to-let properties to supplement, or even replace, their stocks and shares-based pension.

However, the amount of work and expenses associated with maintaining a rental property can be underestimated and too many people invest in buy to let properties with their wallets open and eyes shut.

There are a host of costs to factor in, and also it takes time to attend to the admin and upkeep of the property.

Things like letting agents fees, which range from under 10 to over 20% of the rent[2], accountants’ fees, void periods where the property is empty, maintenance and repairs, the cost of vetting potential tenants (there is now a fine of up to £3,000 if your tenants are not legally allowed to be in the country[3] ), and a host of other legal obligations all need to be considered. It can be a lot more work than many people think.

[1] Source – RBC Brewin Dolphin using FTSE All Share for stock market data, ONS Private Housing Rental Index for rent price and Nationwide house price index. Rent is calculated as a 5% return from concurrent house prices and any previously generated cash, discounted yearly for inflation. Neither stock market data or buy-to-let return include fees.

[2] Using a letting agent, Which?

[3] Penalties for illegal renting, GOV.UK

The value of investments and any income from them can fall and you may get back less than you invested.

Past performance is not a guide to future performance.

No investment is suitable in all cases and if you have any doubts as to an investment’s suitability then you should contact us.

The opinions expressed in this publication are not necessarily the views held throughout RBC Brewin Dolphin Ltd.

We do not give or provide mortgage advice.

Please note that this document was prepared as a general guide only and does not constitute tax or legal advice. While we believe it to be correct at the time of writing, RBC Brewin Dolphin is not a tax adviser and tax law is subject to frequent change. Tax treatment depends on your individual circumstances; therefore you should not rely on this information without seeking professional advice from a qualified tax adviser.